If you think about it… your credit score may be the most important set of numbers in your life. Those numbers affect whether you get approved for a loan or credit card, and they also determine how much interest you will pay when you need to borrow money for a large purchase such as a house or a car. Landlords and employers often access your credit report to determine how reliable of a tenant or employee you may be.

So it is obvious, keeping that score as high as possible is a to your best interest. Your credit score can range anywhere between 300 and 850. Anything higher than a 700 is considered “good,” while the “bad” credit range is anything under 600.

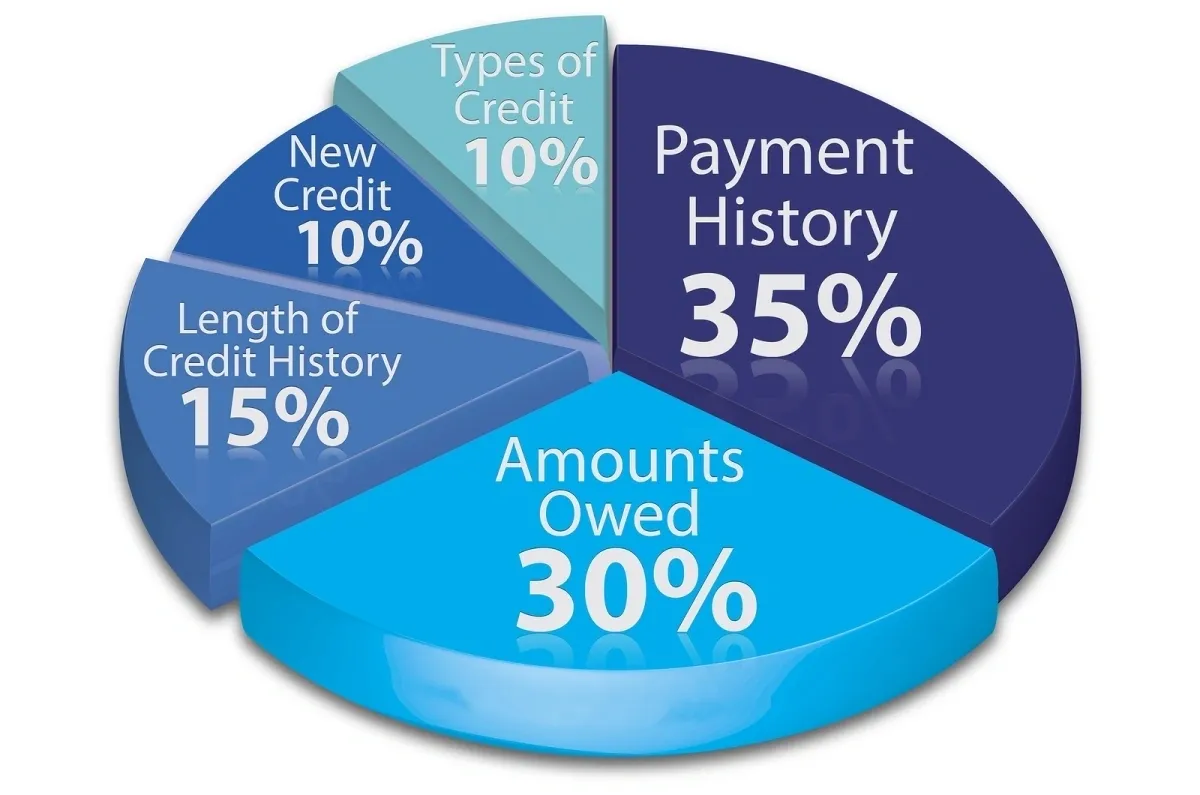

There are five different categories of information utilized to calculate your credit score, each one with a different ranking of importance.

Here’s how each category of credit affects your score:

- Payment History: How frequently you pay your bills on time accounts for 35% of your credit score.

- Credit Utilization: The amount of debt you owe to creditors and lenders makes up 30% of your credit score.

- Length of Credit History: How long you’ve had access to credit is worth 15% of your score.

- Credit Mix and Inquiries: The diversity of the types of credit you have and the number of inquiries you’ve had in the last two years each account for 10% of your credit score.

As you can see, the amount of debt you carry or credit utilization is the second most important component of your credit report. This ratio calculates the amount of money you’ve borrowed through both loans and credit cards and compares it to your actual credit limits. From there, credit utilization can be broken down even further.

It takes into account how much debt you still owe; how many actual accounts have money owed on them; how much you owe on each account; the percentage of revolving credit lines; the percentage of installment loan debt; and potentially the lack of certain kinds of loans.

All of these items combine to contribute nearly one-third of your credit score. So if you want to improve your credit score, you’re going to have to pay attention to your credit utilization.

How Credit Utilization is Calculated

The most important factor when considering your credit mix is just how much debt you have on revolving accounts compared to the maximum amount you’re allowed to charge. This is referred to as your credit utilization ratio (also referred to as balance-to-limit ratio or debt-to-credit ratio.) It’s a very simple calculation to figure it out.

Start by tallying up all of your debts, then separately tabulate all of your credit limits. Then divide the amount of debt by the total credit limits and you have your credit utilization ratio. So if you have two credit cards with a combined limit of $5,000 and you owe $1,000, your calculation would be 1,000 / 5,000. You get 0.20, which means your credit utilization ratio in this scenario is 20%.

Remember that credit utilization is calculated using all of your debts spread out across all of your spending limits. So when you pay off one credit card, should you automatically close the account?

No! This action can hurt your credit score very quickly because taking away an entire line of credit will actually increase your credit utilization ratio — the exact opposite of what you want to do. Here’s how that happens.

Let’s go back to the example where you owe $1,000 and have $5,000 in total card limits. Say each card has a limit of $2,500 but your $1,000 balance is just on one card. If you close the balance-free card, your credit limit drops to $2,500.

Instead of having a 20% credit utilization ratio, the new calculation shows that your ratio has instead jumped up to 40% — that’s double your initial score! Once that happens, your credit score will inevitably drop.

Revolving Debt vs. Installment Debt

When talking about how you utilize credit, it’s important to understand the different types of debt you might have on your credit report. Revolving debt like credit cards and store cards are weighed more negatively than installment loans such as mortgages, student loans, and auto loans.

There are a few different reasons for this. One is that installment loans like those on your house and car have collateral attached to them. If you stop making payments, the lender can foreclose on the home or repossess the car. That makes people more likely to repay those loans before any other type of debt. It also helps the lender recoup the loss of the loan payments.

Student loans don’t have collateral, but they do indicate to lenders that as a borrower you might have a higher capacity for earning potential over time. Revolving debt from credit cards, on the other hand, has no collateral attached to it.

Lenders believe that you’d be less likely to pay on it if you came into financial hardship because you have nothing to lose (except your good credit score). Some installment loans like mortgages and student loans are typically viewed as being “good debt” because they can add value to your income and net worth.

So when your credit score is calculated, it takes into account not just how much debt you have, but what kind of debt you have. This knowledge can help you focus your goals if and when you decide to aggressively pay off your debts.

It’s best to start off with anything owed on a credit card or retail card because not only do they typically carry higher interest rates, they also are weighted more heavily when your credit utilization ratio is calculated for your credit score.

Getting the Best Credit Utilization Score

So now you have the information you need to figure out your credit utilization ratio. How does it look? Most financial experts recommend owing no more than 30% of your credit limit. So if your credit card maximums total $5,000 you wouldn’t want to owe more than $1,500.

Of course, if you pay off your balance in full each month, it’s fine to charge that amount. However, understand that when you’re applying for a loan or credit card, it may very well show your average balance even if you pay it off regularly.

To get around this technicality, you can do one of two things. Either stop using your credit cards for at least a month before submitting a financing application or pay on your account multiple times a month so the balance never looks too high. That’s especially helpful if you rely on any of your cards for some type of rewards program.

If you do regularly carry a balance on your credit cards, and it’s around or above 30% of your overall credit limit, there are still some things you can do to help boost your credit score. The most obvious one is to pay off your debt as aggressively as possible. This will increase your score in a variety of categories, but especially in the credit utilization category.

Remember the subcategories of credit utilization: not only does your credit score consider the overall ratio of your credit spending, it also factors in each individual line of credit.

So, if you’ve maxed out one card and don’t have much charged on the others, focus on getting the high balance card paid down first. There are many other strategies for how to pay down credit card debt, but this is the best one for getting your credit score to increase as quickly as possible.

Opening New Lines of Credit

Another trick of the trade to lower your credit utilization score without actually paying down extra debt is to open up a new line of credit. By adding a new credit card, you’ll automatically have a higher overall limit. Of course, each inquiry for a new credit card or loan application has the potential to temporarily lower your score between 5 and 10 points, so be careful how often you do this.

If you already have a lot of inquiries on your credit report, this may not be looked on favorably by lenders. But if you haven’t had any hard inquiries in the last two years, getting another credit card to use responsibly (or not at all) could alter your credit score in the right direction.

One last red flag lenders look for on a credit report is when you have too many balances spread out across several cards. Yes, that individual credit utilization limit looks lower, but the fact that you’re constantly charging multiple cards can be worrying to an underwriter reviewing your loan or credit card application.

Another strategy to address this issue is to pay down the smallest card first so that you clear an entire line of credit quickly.

Figuring out your credit utilization ratio may seem daunting at first, but no matter what the technicalities may be, simply paying down your debt is often the best way to improve your credit score.

If you would like a 100% Free Professional Forensic Credit Restoration Audit of your Credit, or sign up for one on our website: https://editmycredit.net